Understanding the Key Differences Between These Two

Medicare Paths

One of the biggest decisions Medicare beneficiaries face is choosing between:

● Medicare Advantage (Part C) OR

● Original Medicare with a Medigap Supplement

Both options help cover healthcare costs, but they work very differently.

Choosing the wrong path for your healthcare needs, travel habits, doctors, or budget can lead

to:

● Unexpected out-of-pocket costs

● Network restrictions

● Coverage frustrations

● Higher long-term expenses

There is no universally “best” option.

The right choice depends on:

● Your health

● Budget

● Prescription needs

● Doctor preferences

● Travel habits

● Risk tolerance

This guide explains how Medicare Advantage and Medigap work, their pros and cons, and the

most important differences seniors should understand before enrolling.

First: What Is Original Medicare?

Original Medicare includes:

● Medicare Part A (Hospital Insurance)

● Medicare Part B (Medical Insurance)

Original Medicare is administered directly by the federal government.

However, Original Medicare does not cover all healthcare costs.

Beneficiaries are still responsible for:

● Deductibles

● Coinsurance

● Copays

● No annual out-of-pocket maximum

This is where Medigap supplements may help.

What Is Medigap?

Medigap, also called:

Medicare Supplement Insurance

Is private insurance designed to help pay some of the out-of-pocket costs left behind by Original

Medicare.

Depending on the plan, Medigap may help cover:

● Copays

● Coinsurance

● Deductibles

● Excess charges

With Medigap:

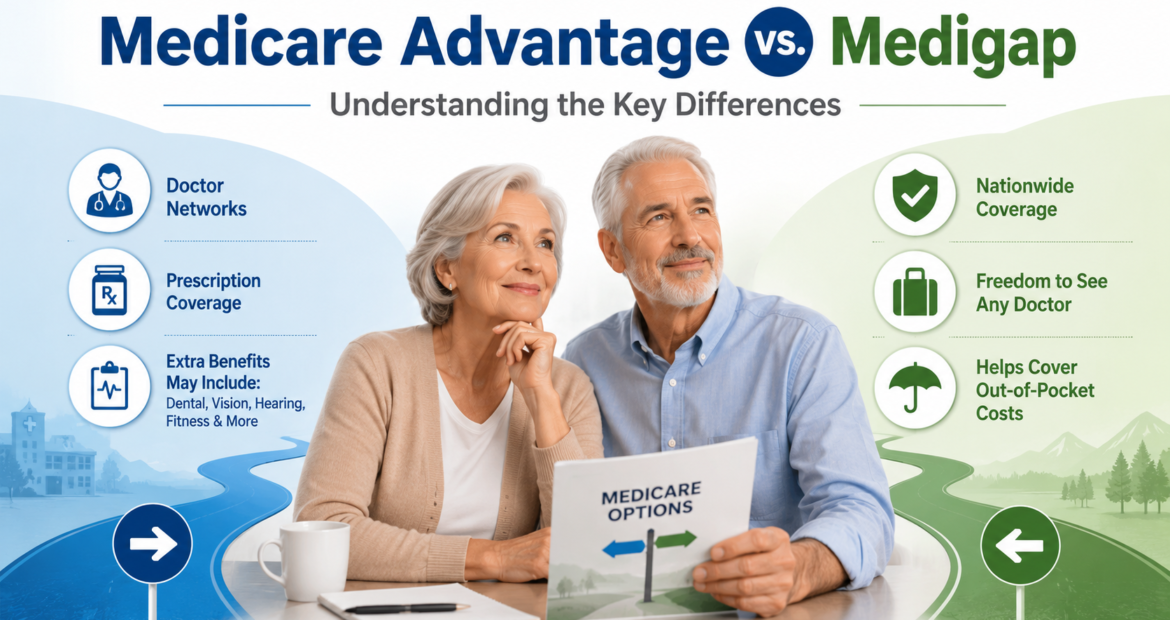

● You generally keep Original Medicare

● You can usually see any doctor nationwide who accepts Medicare

● Referrals are usually not required

Prescription drug coverage is not typically included, so beneficiaries usually purchase a

separate:

Medicare Part D prescription drug plan

What Is Medicare Advantage?

Medicare Advantage, also called:

Medicare Part C

Is an alternative way to receive Medicare benefits through private insurance companies

approved by Medicare.

Most Medicare Advantage plans include:

● Hospital coverage

● Medical coverage

● Prescription drug coverage

Many plans may also offer extra benefits such as:

● Dental

● Vision

● Hearing

● Fitness programs

● Transportation assistance

However, Medicare Advantage plans often use:

● Provider networks

● Referral requirements

● Prior authorization rules

Side-by-Side Comparison Chart

Feature Medicare Advantage Medigap + Original Medicare

Coverage Type Private Medicare replacement

plan

Supplement added to Original

Medicare

Doctor Access Usually network-based Usually any provider nationwide

accepting Medicare

Referrals Often required for specialists Usually not required

Prior Authorization Common Rare for Medicare-covered

services

Prescription Drug

Coverage

Usually included Usually purchased separately

through Part D

Monthly Premiums Often lower upfront premiums Higher monthly premiums

generally

Out-of-Pocket Costs Pay-as-you-go copays and

coinsurance

More predictable costs depending

on plan

Annual Out-of-Pocket

Maximum

Yes Original Medicare itself has no

cap, but Medigap reduces

exposure (many have a MOOP)

Travel Flexibility Limited outside service area in

many plans

Strong nationwide flexibility

Extra Benefits Often includes dental, vision,

hearing

Usually focused on medical

cost-sharing only

Underwriting Later Not usually applicable May require health underwriting

after initial enrollment period

Emergency Coverage

While Traveling

Depends on plan Some Medigap plans include

foreign travel emergency benefits

Plan Stability Benefits and networks can

change yearly

Benefits standardized by plan type

in most states

Best Fit For Budget-conscious beneficiaries

comfortable with networks

People prioritizing flexibility and

predictable costs

The Biggest Difference: Networks vs.

Flexibility

For many seniors, the biggest difference comes down to:

Flexibility versus managed care.

With Medigap:

● You can generally see providers nationwide who accept Medicare

● Networks are usually not a major issue

● This is attractive for travelers and snowbirds

With Medicare Advantage:

● Plans often use local provider networks

● Out-of-network care may cost more or not be covered except in emergencies

● Referrals and prior authorization may apply

Medicare Advantage Pros

Lower Monthly Premiums

Many Medicare Advantage plans have:

● Low premiums

● Sometimes even $0 premiums

Though beneficiaries still pay the Medicare Part B premium.

Extra Benefits

Many plans include:

● Dental

● Vision

● Hearing

● Gym memberships

● Over-the-counter allowances

These benefits are attractive to many seniors.

Built-In Prescription Drug Coverage

Most Medicare Advantage plans include Part D drug coverage.

This creates a more bundled insurance experience.

Annual Out-of-Pocket Maximum

Unlike Original Medicare alone, Medicare Advantage plans include yearly out-of-pocket

spending limits for covered medical services.

Medicare Advantage Cons

Provider Networks

You may need to:

● Stay in-network

● Change doctors

● Get referrals

This can create limitations for some beneficiaries.

Prior Authorization Requirements

Certain:

● Procedures

● Tests

● Treatments

● Medications

May require insurance approval before coverage applies.

Costs Can Add Up During Serious Illness

Although premiums may be lower, repeated copays and coinsurance can become expensive

during years with major medical needs.

Plans Change Annually

Benefits, formularies, provider networks, and copays can change each year.

Annual plan reviews are important.

Medigap Pros

Broad Doctor Access

One of the biggest Medigap advantages is provider flexibility.

Many beneficiaries appreciate being able to:

● Travel freely

● Use specialists without referrals

● Access major medical centers nationwide

Predictable Costs

Depending on the Medigap plan selected, out-of-pocket healthcare expenses may become far

more predictable.

Some plans cover most Medicare-approved cost-sharing.

Fewer Authorization Issues

Original Medicare generally does not require the same level of prior authorization commonly

seen in Medicare Advantage plans.

Stability

Medigap benefits are standardized by plan letter in most states.

That means a Plan G from one company provides the same core benefits as a Plan G from

another company.

Medigap Cons

Higher Monthly Premiums

Medigap plans often cost more upfront each month.

This can be difficult for budget-conscious seniors.

Separate Drug Plan Needed

Beneficiaries usually must purchase a standalone prescription drug plan (Part D) separately.

Fewer Extra Benefits

Most Medigap plans focus on medical cost-sharing rather than:

● Dental

● Vision

● Hearing

● Grocery cards

● Fitness extras

Medical Underwriting Later On

In many states, if you apply for Medigap outside your guaranteed enrollment window, insurers

may use:

● Health underwriting

● Medical questions

● Coverage denial in some situations

This is one reason timing matters.

What Is the Best Time to Enroll in

Medigap?

The best time is generally during your:

Medigap Open Enrollment Period

This usually begins when:

● You are 65 or older

● Enrolled in Medicare Part B

During this window, insurers generally cannot deny coverage due to health conditions.

After this period, underwriting may apply in many states.

Can You Switch Between Medicare

Advantage and Medigap Later?

Sometimes, but there can be challenges.

Switching from:

Medicare Advantage to Medigap

May require medical underwriting depending on:

● State rules

● Timing

● Health conditions

Some beneficiaries later discover they cannot qualify for affordable Medigap coverage after

developing health issues.

This is an important long-term consideration.

Medigap to Medicare Advantage

Can be completed during:

● Annual Enrollment Period (AEP) August 15-December 7 effective January 1st

● Special Enrollment Period (triggered by a qualifying life event)

Which Option Is Better for Travelers?

Generally:

Medigap offers greater nationwide flexibility.

This is especially valuable for:

● Snowbirds

● RV travelers

● People splitting time between states

Many Medicare Advantage plans operate primarily within local service areas.

Questions Seniors Commonly Ask

“Can I Have Both Medicare Advantage and Medigap?”

No.

You generally cannot use a Medigap policy with a Medicare Advantage plan.

“Do Both Options Cover Prescriptions?”

Medicare Advantage often includes drug coverage.

Medigap usually requires separate Part D enrollment.

“Are Medicare Advantage Plans Free?”

Not exactly.

Even $0 premium plans still require:

● Medicare Part B premiums

● Copays

● Deductibles

● Coinsurance

“Can Medicare Advantage Deny Care?”

Plans may require prior authorization for certain services before coverage approval.

“Can Medigap Premiums Increase?”

Yes.

Premiums may rise over time based on:

● Age

● Inflation

● Insurance company pricing structures

How to Choose Between Medicare

Advantage and Medigap

Consider:

● Your monthly budget

● Doctor preferences

● Prescription needs

● Travel habits

● Tolerance for networks and referrals

● Long-term healthcare risks

There is no one-size-fits-all answer.

The best plan depends on your personal priorities.

Final Thoughts

Medicare Advantage and Medigap represent two very different approaches to Medicare

coverage.

Medicare Advantage often emphasizes:

● Lower upfront costs

● Bundled benefits

● Managed care networks

While Medigap focuses more on:

● Provider flexibility

● Predictable medical costs

● Nationwide Medicare access

Both options can work well depending on the beneficiary’s health needs, budget, and lifestyle.

The most important step is understanding the tradeoffs before enrolling.

Comparing plans carefully and reviewing your healthcare priorities can help ensure your

Medicare coverage suits your needs. Speak to one of our licensed insurance agents today to

give more in depth information and answer any questions you have.